Early Retiree Reinsurance Program

Early Retiree Reinsurance Program

SUCCESSFUL SUPPORT OF EARLY RETIREE HEALTH COVERAGE

Program Background and Purpose

The Early Retiree Reinsurance Program (ERRP) was included in the Affordable Care Act (ACA)1 to provide financial assistance to employment-based health plan sponsors—including for-profit companies, schools and educational institutions, unions, State and local governments, religious organizations and other nonprofit plan sponsors—that make coverage available to millions of early retirees and their spouses, surviving spouses, and dependents. Prior to January 1, 2014, when guaranteed issue of insurance coverage, elimination of preexisting condition exclusions, and several other critical ACA protections took effect for individual health insurance coverage, early retirees between ages 55 and 64 often faced difficulties obtaining insurance in the individual market because of age or chronic conditions that made coverage unaffordable or inaccessible. These early retirees were often charged more for health coverage based on their health status, or denied coverage altogether in the individual market. Early retiree health coverage through employment-based plans provides a valuable bridge from employment coverage, for active workers, to Medicare coverage, for eligible retirees. Over the past 20 years, however, the availability of group health coverage for America’s retirees has declined significantly. The percentage of large employers providing workers with retirement health coverage has dropped from 66 percent in 1988 to 29 percent in 2013.2

The ERRP was designed to help employers and other sponsors of employment-based health plans continue to provide coverage for early retirees until 2014, the initial year under the ACA in which insurance companies may no longer deny coverage based on pre-existing conditions, or charge more based on an individual’s health status. Established by section 1102 of the ACA which was enacted on March 23, 2010 (Pub. L. 111-148), ERRP provided financial assistance for employment-based health plan sponsors to help early retirees and their spouses, surviving spouses, and dependents maintain access to quality, affordable health coverage. Plan sponsors that were accepted into the program could receive reinsurance reimbursement for a portion of the claims for health benefits for early retirees age 55 and older who were not eligible for Medicare, and their spouses, surviving spouses, and dependents.

Program Participation

What types of organizations participated?

Commercial, non-profit, union, and religious organizations, as well as state and local governments,3 participated in the ERRP. State and local governments, the largest of which are more likely than the largest private employers to offer retiree health benefits,4 represented the slight majority of the nearly 2,900 sponsors that received ERRP reimbursement. Participating plan sponsors of this type included States or government subdivisions (e.g., counties, cities, and special districts), school districts, or organizations representing government employees (e.g., teachers and police officers). All types of plan sponsors attempted to maintain affordable health coverage for their active employees and early retirees, while continuing to meet demands for their products and services. ERRP proved to be a critical source of support by benefiting early retirees, their family members, other plan participants, and the health plan sponsors that provided vital access to health coverage. As the program was implemented during the economic recession, there was a significant response from sponsors of retiree health plans.

How much reimbursement did the participating organizations receive?

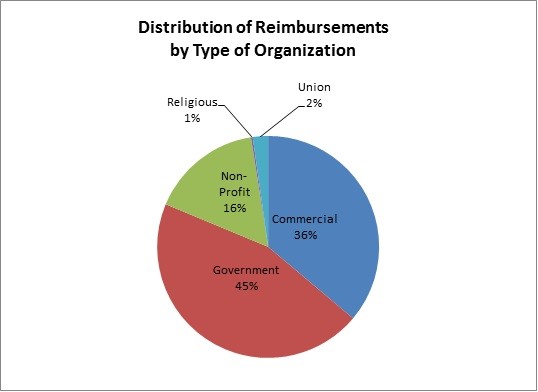

ERRP provided nearly $5 billion in reinsurance payments to approximately 2,900 employers and other sponsors of retiree plans.5 The size of health plans for which plan sponsors received reimbursements varied significantly. However, the median total amount paid per plan sponsor was approximately $190,000, indicating that a sizeable number of small and medium sized plan sponsors were helped by ERRP. Figure 1, below, provides the distribution of program reimbursements by type of organization.

Figure 1

What types of health benefit costs were submitted for reimbursement by participating plan sponsors?

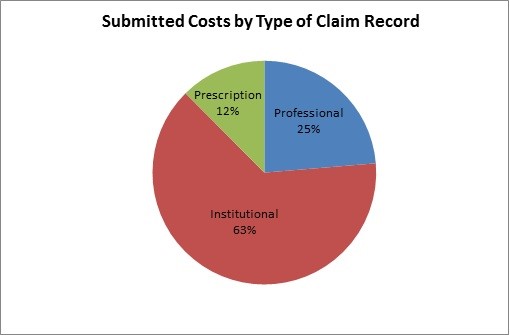

ERRP provided critical support to plan sponsors’ coverage of individuals with high costs and chronic conditions. Based on analysis of claims ERRP received, plan sponsors collectively requested reimbursement for more than 275,000 early retirees, spouses, surviving spouses, and dependents with significant health care costs (i.e., costs exceeding $15,000 in ERRP-eligible health care claims per plan year). A large proportion of ERRP funds were used to reimburse plan sponsors for claims related to chronic and high-cost conditions such as heart disease, cancer, respiratory disorders, arthritis, and diabetes.6

The claim costs submitted by plan sponsors were reported using three types of claims records: Prescription, Professional, and Institutional. Figure 2, below, shows the distribution of reported costs, by type of claim.

Figure 2

How many individuals benefited from sponsors’ receipt of ERRP reimbursements?

A subset of plan sponsors, associated with 1,622 plans 7, that received ERRP reimbursements and responded to 2012 and 2013 voluntary surveys of plan sponsors that had received such reimbursement, indicated that 26 million enrolled individuals, of which almost 2.6 million were early retirees8 , benefited or will benefit from the plan sponsors’ receipt of funds. Due to the fact that additional sponsors, associated with 1,446 plans, received ERRP funds and did not respond to the voluntary surveys, it is not possible to determine the exact number of individuals who benefited from plan sponsors’ receipt of ERRP reimbursements. However, it is likely that many millions of additional individuals, beyond the 26 million, reaped or will reap the important benefits of ERRP.

How did individuals and plan sponsors benefit from plan sponsors’ receipt of ERRP reimbursements?

Plan sponsors used ERRP funds to significantly relieve the burden of the high cost of health coverage to themselves and their plan participants. For example, of the plans that reported in the 2012 and 2013 surveys that they spent ERRP funds during their 2011 plan year, 56% reported that they used such funds to offset increases to their health benefit claim costs, and that they offset such costs increases by an average of 42%. Of the plans that reported that they spent ERRP funds during their 2012 plan year to reduce or offset increases to their individual plan participant’s premium costs, these plans reported that participants paid premiums that were on average 40% less than what they would have paid, absent ERRP.

Summary

ERRP proved to be a valuable source of support, benefiting early retirees, their spouses, surviving spouses, and dependents, and the health plan sponsors that provided vital access to health coverage. Plan sponsors that responded to the surveys reported that they provided health coverage to nearly 26 million plan participants, of which almost 2.6 million were early retirees. Without the early retiree health coverage that was supported through the ERRP, many early retirees might not have had any actual or affordable alternatives prior to the ACA health insurance reforms that took effect in 2014. The response from employment-based health plan sponsors to the ERRP was not surprising given the significant health care costs experienced by early retirees and plan sponsors. In addition, the response highlights the importance of programs, such as those established by the ACA, in supporting the availability of private health coverage.

Questions

If Plan Sponsors have questions about general ERRP requirements (e.g., record retention, appropriate use of funds), they may send an email to ERRP@cms.hhs.gov.

_________________________

[1] Patient Protection and Affordable Care Act (Public Law 111–148).

[2] Kaiser Family Foundation, The Kaiser Family Foundation and Health Research & Educational Trust: Employer Health Benefits 2013 Annual Survey, http://kff.org/private-insurance/report/2013-employer-health-benefits/.

[3] Each plan sponsor self-reported their type of organization in their ERRP application./.

[4] Kaiser Family Foundation, The Kaiser Family Foundation and Health Research & Educational Trust: Employer Health Benefits 2013 Annual Survey.

[5] Approximately 2 percent of the $5 billion ERRP appropriation was used to cover program administrative costs.

[6] CMS identified these conditions by determining the principal diagnosis codes associated with high, aggregated paid claim amounts submitted for reimbursement by ERRP-participating plan sponsors.

[7] A plan sponsor may be associated with one or more health plans.

[8] The 2.6 million “early retirees” (as defined in 45 CFR Section 149.2) are comprised of early retirees, spouses, surviving spouses, and dependents.

Additional Resources:

Page Last Modified:

09/06/2023 05:05 PM